The primary task of microeconomics is to study prices and production in the market. There is an interaction between the different markets in the economy. The study of interaction between markets is under the realm of microeconomics. But the economy wide aggregate is the study of macroeconomics. As a result, the scope of microeconomics is to study the market from the individualistic point of view.

Microeconomics Concept

Microeconomics studies the allocation of resources in the economy. Proper allocation of resources ensures the productivity of resources. As a result, the efficiency in the economy will also increase.

Demand

Demand is an important concept of microeconomics. It refers to the commodity that a buyer wants to purchase backed by purchasing power. Here the main keywords are want and purchasing power. For demand to complete in the economy only want cannot be the factor. It has to be backed by purchasing power of the commodity. Because demand will be complete if the commodity is transferred from the seller to the buyer after paying the price of that commodity.

Demand theory in the economy is the basis of the law of demand and the demand curve. It states the relation between the customer desire and the amount of goods that are available. The main concepts of demand are desire, willingness and the price to pay for the product. All the three concepts are interconnected. Demand as a concept focuses on all the three heads. Because they are interconnected, demand will not be complete if one is missing.

As a consumer of the product the foremost important part of demand is desire for a certain product. Desire is the want that arises after seeing a product in the market. Willingness for the product is second. Because the desire is affirmative there has to be willingness to purchase the product. The third concept is very important i.e. price to pay. If the buyer does not have the purchasing power then the demand will not be complete. As a result, the demand becomes complete if all three concepts fall in line in the economy.

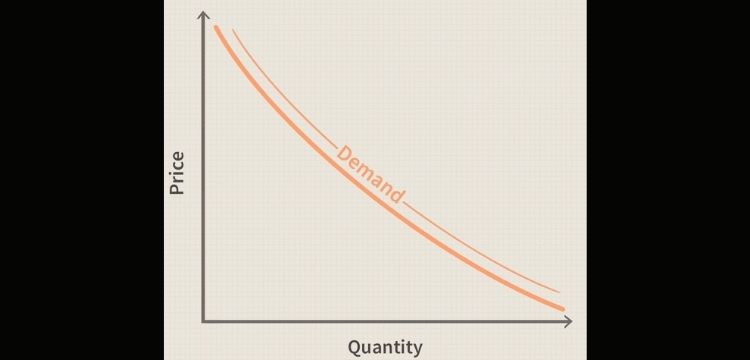

Demand Curve

The demand curve in microeconomics is the graphical representation of the relation between price of commodities and quantity demanded in the economy. The price of the commodity is marked on the Y-axis. The quantity demanded is marked on the X-axis. The graph represents the inverse relation between price and quantity demanded.

The demand curve is downward sloping as it shows the negative relation between price and quantity demanded.

Law of Demand

The law of demand states that when the price of the commodity increases the quantity demanded will decrease. The law of demand states the inverse relation between the two attributes in the economy.

When the price of goods and services increase the demand for the commodity decreases. But when the price of goods and services decrease the demand for the commodity increases in the economy.

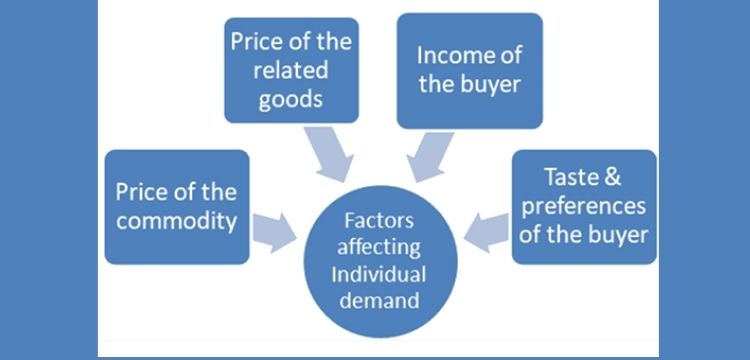

Factors affecting Demand in Microeconomics

Demand for a commodity in the market depends upon many factors. Price, income, prices of related goods all affect the law of demand in some way or the other.

Price

The price of a product affects the demand of the commodity in the market. When the price of a product is high then the quantity demanded will be low. As a result there will be a shift along the demand curve. When the price of a product is low then the quantity demanded will be high. In this case too there will be a shift along the demand curve. The law of demand also states that when price increases the quantity demanded declines.

Income affects Microeconomics

Income of a consumer also changes the level of demand in the economy. When the income of the consumer rises then the demand for goods and services in the economy increases. This will shift the demand curve rightwards indicating that the demand has increased. When the income level of the consumer decreases then the demand for commodities decreases. The demand curve shifts leftwards indicating that the demand for goods and services have decreased.

Price of Related Goods

Prices of related goods affect demand in a drastic way. Related goods can be substitute goods or complementary goods.When prices of certain goods change it affects the demand of other goods as well.

In the case of substitute goods, if the price of a commodity increases, the demand for the substitute good will increase. For example tea and coffee are substitute goods. When the price of tea increases then the demand for coffee in the market will rise. Because the price of tea is higher than the price of coffee.

In the case of complementary goods the demand for the product will depend on the prices of the commodity. For example, cars and petrol are two complementary goods. If prices of petrol increase the demand for cars will decrease.

Taste and Preference

The taste and preference of the customers related to the choice of goods matter in the economy. The taste and preference for a product is a personal affair. As a result it depends on the psyche of the person. Taste and preference changes from time to time. If the preference for a product changes then the demand for that quantity will increase or decrease. Preference for a product depends on various factors like price of the commodity or the income of the person. If the price increases then the customer will prefer another product. If the income of the consumer increases then he will prefer luxury goods rather than inferior goods.

Expectations in change of price

Another factor that affects the law of demand is the expectation of rise in price of the product. A consumer will increase the demand for the product if he expects the price of the commodity to rise. This fluctuation in demand in the market will automatically cause a rise in price level due to the interaction of the market forces.

Exceptions to demand in Microeconomics

As the law of demand states that when the price of a commodity increases the demand for the commodity will decrease. But there are certain exceptions to the rule in certain cases. As a result in these cases the law of demand does not work efficiently. Because with change in price or income of the consumer the demand for these goods will decrease, increase or there will be no change.

Necessary Goods

Necessary goods are those goods that are consumed daily or it is used for daily household purpose. Salt is the best example of necessary goods in the economy. In this case if the income of the consumer increases then the quantity demanded of salt will remain the same. At the same time if the price of salt increases then also the quantity demanded will remain the same. Therefore in the case for necessary goods the price or income of the customer does not affect the demand for the product. It will remain the same.

Giffen Goods

Giffen goods are the inferior goods in the economy. In case for inferior goods the price or income of the customer does not matter. If the price of the inferior goods rise then there will be no effect on the quantity demanded of the commodities. At the same time, when prices of inferior goods decrease the effect on quantity demanded will remain the same.

When income of the consumer increases then the quantity demanded of the commodity will decrease. The law of demand in this case does not hold true. As a result with increased income the demand for these products decrease.

Veblen Goods

Economist Thorstein Veblen gave the concept of Veblen goods in the economy. This concept works on the principle of conspicuous consumption. In these cases as the prices of goods increase the demand for the commodities will also increase. Gold is an example of Veblen goods. In the market when the price of gold increases then the market demand of gold will also increase. The law of demand does not function in cases of Veblen goods.

Elasticity of Demand

The elasticity of demand is an important concept in microeconomics. Elasticity of law of demand can be classified into elastic demand, inelastic demand and unitary demand.

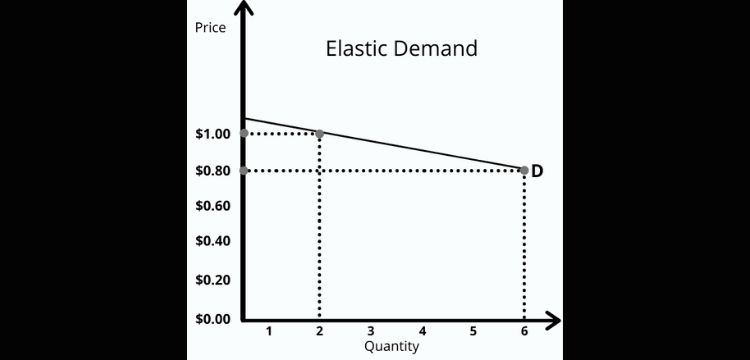

Elastic Demand

Elastic demand refers to when the change in quantity demanded is more than the change in price level in the market. With a small change in price in the economy the quantity demanded change is more. Consumer durable goods have elastic demand. The examples of consumer durables are fridge, washing machines etc. If the price increases for these products then the demand to purchase them will postpone.

Close substitutes goods also affect the elasticity of demand. If the price increases for a product then the consumer will shift to another commodity in the market.

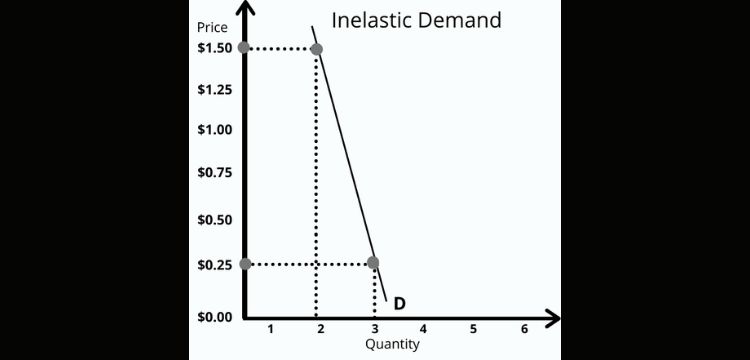

Inelastic Demand

Inelastic demand refers to when the price change of the commodity in the market is higher than the change in quantity demanded. Quantity demanded of the commodity does not change much as compared to the price of the commodity. An example of inelastic demand is that of food grains. If the prices of food grains increase then the demand for the same will not decrease. The consumption of food remains the same irrespective of the rise in price.

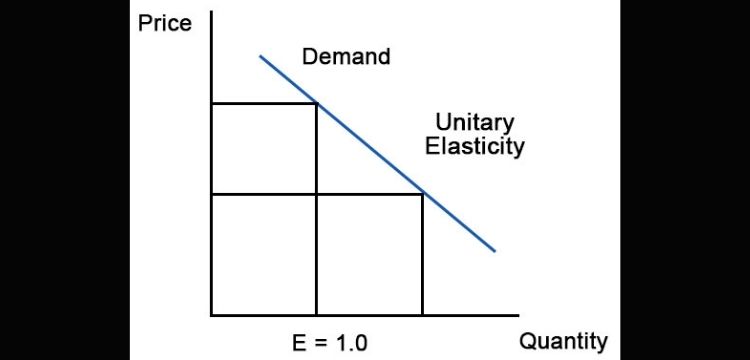

Unitary Elastic Demand

When the elasticity of demand is equal to one then the demand curve is unitary elastic. In this case the change in price and change in quantity demanded is the same. An example of unitary elastic demand is of digital cameras. When the price of a digital camera decreases by 10% then the quantity demanded of the same increases by 10% in the economy.

Supply

Supply is the total amount of goods or service that is available to consumers in the economy. The supply of a commodity will rise if the price of the product rises. Because all firms try to maximize their profits.

The concept of supply in microeconomics is complex. While supply can refer to anything that is sold in a market. One of the important factors that affects supply is the price of the commodity. As a result if the price of the commodity increases the supply will also increase. The price of related goods, input price also affect supply. As a result, the cost of production also increases. When the cost of production increases the price of goods and services will also increase. As a result the supply of commodities in the market increases.

The change in technology increases the quality of the product. When the quality of product increases the price will also increase. Government regulations can also affect supply. Environmental laws, the number of suppliers and market expectations can cause change in supply in the market. An example of this is when environmental laws affect the supply of oil and the price in the global market.

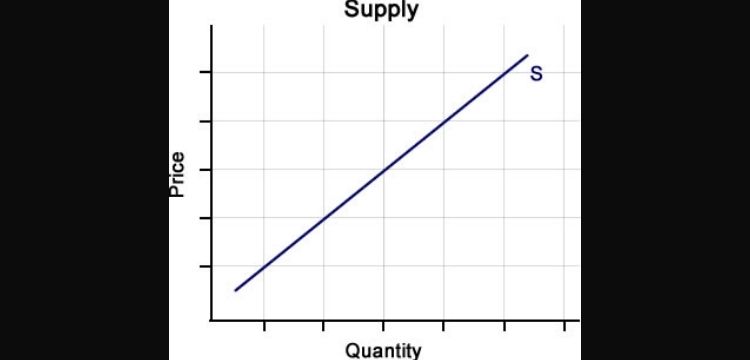

Supply Curve

The supply curve is an upward sloping curve. The graph shows the positive relation between price and quantity supplied in the economy. The price of the commodity is marked on the Y-axis. The quantity supplied in the market is marked on the X-axis. The graph represents the positive relation between price and quantity supplied.

Law of Supply

The law of supply is the microeconomics states that, all other factors being equal, when the price of goods and service increases, the quantity of goods or services supplied will increase. But when the price of goods and services decrease the quantity supplied will decrease.

The law of supply says that when the price of the commodity rises in the economy, suppliers will try to maximize their profits by increasing commodities that are offered for sale.

Factors affecting Supply in Microeconomics

There are a number of factors that affect the supply of goods and services in the economy.

Price

Price is an important factor that affects the supply of goods in the economy. When the price of goods are high the supply of the products are also high. At the same time when the price of goods are low the supply of the commodities will be low. Traders try to maximize profits by selling their products at a high price when the commodities in the market are low. When the supply of goods is low and the demand is high the products will be costly. As a result the traders will earn higher profits by selling the goods and services.

Cost of Production

Cost of production is another factor that affects the supply of goods and services in the economy. The factors of production are land, labour, capital and entrepreneur. When the price of the factors of production increase the cost of production will also increase. This will cause the supply of the goods to shrink to save the resources in the economy. Traders and manufacturers try to hoard the goods till the market price is exceeded.

Technology

The increase in supply is the result of advancement in technology that decreases the cost of production. Technological development improves the efficiency and productivity that reduces the cost of production.

Government Policies

Government plays an important role in controlling the supply of commodities in the economy. They try to regulate and protect the market against false creation of demand and supply. Tax policies affect the market supply. The lower will be the tax the higher will be the supply of that product in the market. As a result if the strict regulations and the excise duty is imposed then the supply of the product will decrease.

Transport

The transportation of raw materials from one place to another is essential in ensuring the proper supply of the product in the economy. Poor transport facilities are a hurdle to the supply of products. Because the products are not available on time in the market. Without the proper transport system raw materials cannot be delivered to the manufacturer. The lack of transport facilities will prevent the manufacturer in proper distribution of the product. This will affect the company’s urge to earn high profits. As a result the competitiveness of the company will also be affected.

Exceptions to the Law of Supply

There are certain exceptions to the law of supply in the economy. As the law of supply states that when the price of a commodity increases the supply for the commodity will increase. But there are certain exceptions to the rule in certain cases. As a result in these cases the law of supply does not work efficiently.

Change in Business

When a manufacturer tries to close his business then he will sell his products at a much lower price. Here the price is low and the supply of goods is high. For this case the law of supply is not being followed.

Supply of Rare Commodities

The supply of rare commodities in the market as a straight line vertical supply curve. In this case the quantity supplied remains the same but the price of the product increases. Here the supply curve is inelastic in nature.

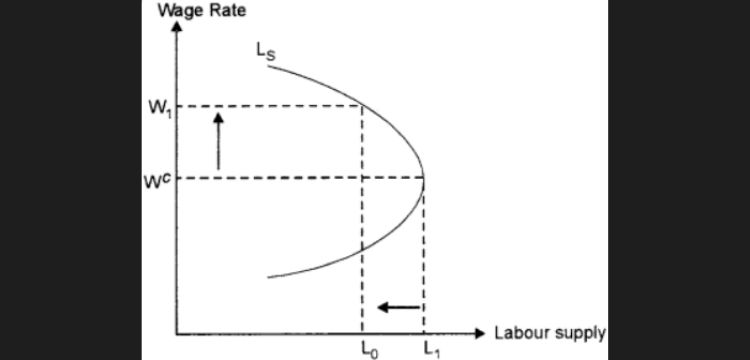

Labour Supply Curve

The law of supply breaks in case of a labour supply curve in the economy. The labour supply curve is backward bending. Because of the functioning of the substitution effect and the income effect.

When the wage rate is low the workers will try to work more. As a result the wage rate will increase. This will cause the labour supply to increase. In this case the substitution effect is stronger than the income effect.

When the wage rate is high the workers will tend to enjoy work less. The importance of leisure comes in the forefront. Here the labour curve is backward bending. There is less supply of labour in the economy causing the curve to bend backward. In this case the income effect is stronger than the substitution effect.

Share Market

The supply curve in the share market is negative sloping. Since share market works are based on uncertainty, people try to anticipate the change in prices. As a result when prices of share decrease people try to sell more to reduce their losses.

Elasticity of Supply

Elasticity of supply is the degree of quantity supplied to a change in it’s own price of the commodity. It can also be defined as the percentage change in quantity supplied divided by the percentage change in price of that commodity.

Determinants of Elasticity in Microeconomics

There are certain factors which affect the elasticity of supply of commodities in the market.

Nature of the commodity

The major determinant of elasticity of supply is the availability of substitutes of the product that is being sold. Substitute goods refers to those factors of production that can easily be transferred. A farmer can substitute from growing wheat to producing jute. When the factors of production are easily transferred from production of one commodity to another then elasticity of supply will be greater. The elasticity of supply for durable goods is high. Elasticity of perishable goods are low.

Time

Time also has an effect on the elasticity of supply. Elasticity of supply is more in the long run than compared in the short run. As a result, when the time period is long it is easier to shift resources on the products.

Price Level

Elasticity of supply changes with the price level. When the price level of a commodity is high the sellers will supply more number of products in the market.

Definition of the Product

The elasticity of supply also depends on the definition of the product. If the product is narrowly defined then the elasticity of supply will be high. If the product is defined in a proper way the elasticity of supply will be low.

Cost of Attracting Resources

When the supply in a market increases the resources are attracted from other industries as well. As a result the price of the resources are increased. When the price of resources rises, the cost of production will increase. As a result the supply will be relatively inelastic. If the price of resources are low the supply will be relatively elastic.

Types of Elasticity of Supply

There are fives types of elasticity of supply in microeconomics. Elasticity of supply is the quantitative relationship between quantity supplied and price. The price elasticity of supply can be represented as percentage change in price divided by percentage change in quantity supplied.

Perfectly Inelastic Supply

A commodity is perfectly inelastic when the given commodity can be supplied irrespective of it’s price. The elasticity of supply is zero. The curve is straight line parallel to Y-axis.

Relatively Less Elastic Supply

When the change in quantity supplied is less than the change in price. As a result, such situation is called relatively less elastic supply. The price elasticity is less than 1.

Relatively Greater Elastic Supply

When the change in quantity supplied is more than the change in price level. In this case, the price elasticity is greater than 1.

Unitary Elastic

The change in quantity supplied is exactly equal to the change in price. Therefore, the change in quantity supplied and price is proportionate. the elasticity of supply is equal to 1. Unitary elastic supply curve passes through the origin.

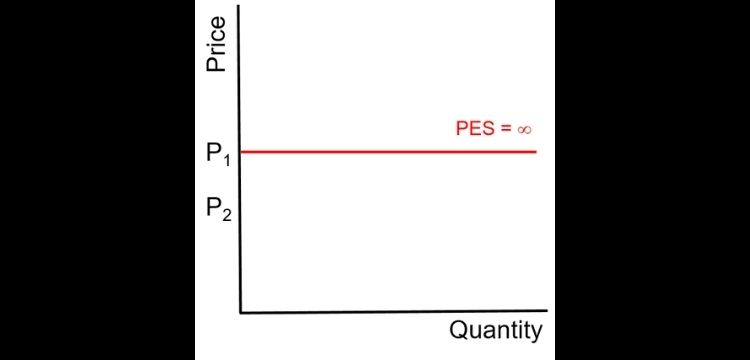

Perfectly Elastic Supply

A commodity with perfectly elastic supply denotes infinite elasticity. Here, the elasticity is zero with a fall in price. When the price rises, the elasticity becomes infinite. It means, suppliers can supply any amount of quantity with a rise in price. It is a straight line parallel to X-axis.

Conclusion

Microeconomics is a very important branch of economics. It deals with both the market forces in the economy. The market forces are demand and supply. Market forces determine the price of goods and services in the economy. In this blog we have seen the factors affecting the market forces in the economy.

When we speak of market forces it becomes important to state the elasticity of demand and supply. In this blog we have studied the elasticity of demand and supply and also the factors that determine the elasticity. Microeconomics studies all the characteristics of the economy individually. The market structure, utility comes under the ambit of microeconomics.

WhatsApp

WhatsApp